Cap-and-Trade

Outline

- Recap on cap-and-trade, instrument choice in theory

- Acid Rain Program

- early evidence on cost-effectiveness

- Fowlie (2010)

Theory recap

Review of the first best

The short run (conditional on $J$ firms) optimality conditions:

- marginal benefits of consumption equal marginal costs

- marginal abatement costs at each firm are equal to aggregate marginal damages

Necessary condition, cost-effectiveness, is the primary motivation for cap and trade.

Cap and Trade

The regulator issues $L$ emission permits

- ideally $L=E^*$, but this is rarely the case

- so we focus on cost-effectiveness instead

If permits are auctioned at clearing price $\sigma$, firm's maximize

Assume the market good price $p$ and emission price $\sigma$ are taken as given.*

Yields FOCs:

Define $e_j^*$ as the optimal amount of emissions for each firm under the cap.

Comparison with an emissions standard

In the simplest case, instead of issuing permits, the regulator fixes the total amount of emissions at each firm, $e_j \le \bar e_j$.

If the regulator simply sets $\bar e_j = e_j^*$ then this policy is equivalent to the cap from an efficiency perspective.

[Note that the regulator loses revenue $\sigma L$ compared to the auctioned permits case].

In practice, emissions standards are typically set on an average

(rather than a firm-specific basis)

For example, if there are $J$ polluting firms, the regulator might set

If firms are heterogenous, then the necessary condition for cost-effectiveness will not be met.

- if firms differ greatly in size, it might not even be binding

[Notes:]

Consider the case where this is binding for all firms.

They maximize

With FOC:

If firms are homogenous, ie

If firms are heterogenous, then the necessary condition for cost-effectiveness will not be met.

- For example with $C^1_e(x_1,\bar e ) < C^2_e(x_2,\bar e )$, the same emission level could be achieved at lower social cost by moving some emissions from 1 to 2.

A more obvious problem is that if firms are very different (for example different sizes)

- then a uniform emission level might not even be binding for some firms, ie $\hat e_j < \bar e$.

A more common approach is to set an emission rate standard.

For example, the regulator could pick a level of emissions per unit $\alpha$, so $e=\alpha x$.

Firms now maximize

With FOC:

Summary: Cap-and-trade vs uniform rate

Can show that a uniform emission standard achieves its E at greater output levels and higher cost than a uniform standard (or a cap)

Intuition: Under a emission rate standard, the firm can "comply" by increasing output.

[Notes:]

- Define the firms output supply function under an intensity standard $x=x(\alpha)$.

- Now imagine the regulator knows this relationship, and picks $\alpha$ such that $\alpha x(\alpha) = \bar e = E^* /X(E^*)$

- (the uniform level emission target from above)

Plugging into the FOC,

Noting that $-C_e() > 0$, we can compare this the FOC from the uniform level ,

From this it is clear that:

- $x(\alpha) > x(\bar e)$

- $-C_e(x(\alpha),\bar e) > -C_e(x(\bar e),\bar e)$

Also note:

How large are the cost savings from from cap-and-trade?

Clearly depends on the shape and distribution in abatement cost functions over the relevant range.

In practice will also depend on

- if permits aren't auctioned, are transaction costs low?

- are actors "rational" (cost-minimizers)?

C&T has been implemented in US leaded gasoline, SO2, and numerous CO2 policies world wide.

For a recent review of major programs to date, see Stavins and Schmalensee (REEP 2019).

For a list of global C&T policies in place, see World Bank 2018.

Acid Rain Program

Title IV of the Clean Air Act Amendments of 1990

Small part of much bigger bill. Basically everything else command and control.

The Cap

- Cut U.S. SO2 emissions by 50% (10 million tons) below 1980 by 2000

- Phase I, 1995-1999, 263 most polluting coal-fired electric generating units

- Phase II, began 2000, 3200 units nearly all U.S. fossil-fueled plants

Target not chosen to maximize net economic benefits

- Chosen to satisfy campaign pledge of George H. W. Bush; believed to be

consistent with “elbow” of the abatement cost curve

Allocation

- Not auctioned

Banking and borrowing

- Permits have a vintage

- Polluters can chose to use more allowances this year and less next year

(borrowing) - Or pollute less this year and save to be able to pollute more next year (banking)

Three compliance options

-

Burn less coal (can just reduce output)

-

Install a scrubber to remove sulfur from emissions

-

Fuel switch to a lower sulfur coal.

Ex ante, people were afraid of 1 and thought 2 was the most important strategy. Ex post it was primarily 3.

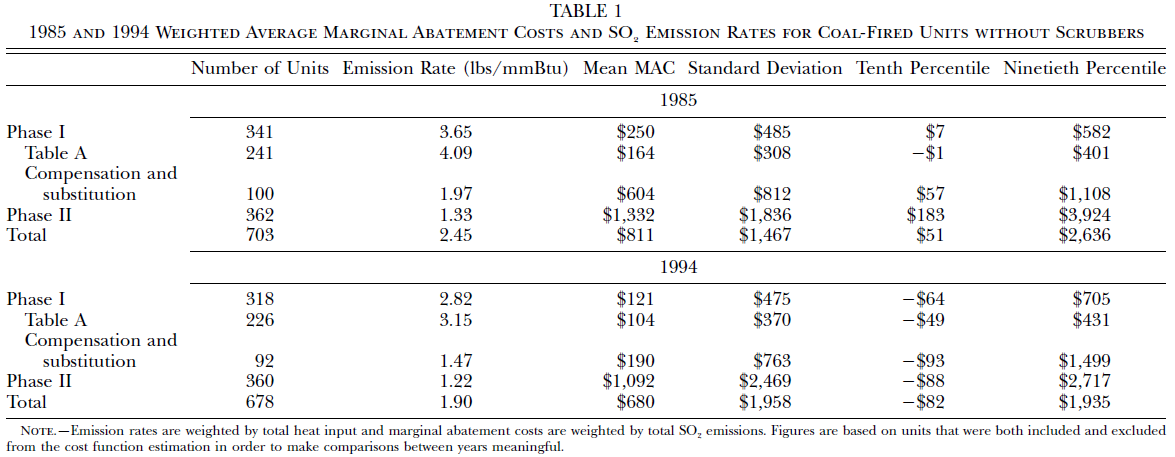

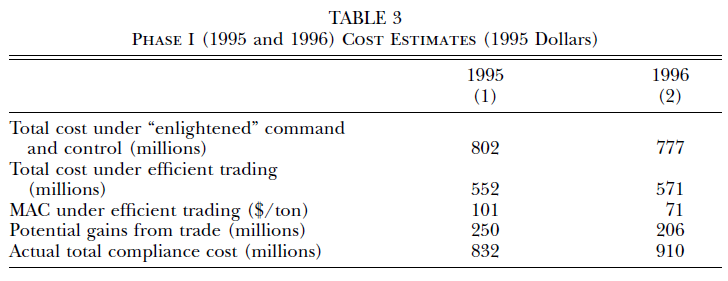

Carlson et al (2000) provide and early and widely cited evaluation of the ARP

Research Questions:

-

How much does cap-and-trade reduce costs, compared to command and control (a uniform standard)?

- How much of heralded cost savings due to program?

-

Are these gains realized immediately? Or does the market take time?

Empirical strategy

-

Estimate cost of producing electricity as a function of output, input, capital and coal type

- using pre ARP data: 1985-1994

-

Hold cost function as fixed and calculate costs of meeting same quantity under alternative policies:

- A technology standard: forced scrubber installation.

- A uniform emission rate standard.

Main results: Cost function

Main results: Cost Effectiveness

Is this the true policy cost?

The abatement cost of going from $\hat e^x$ to $e$ is typically defined as

with the marginal cost of emissions reductions at a given $x$, $C_e(x,e)$.

However, in this setup, with fixed marginal revenue $p$, an increase in costs will also lead to a reduction in output.

Fowlie

AER, 2010

Overview

-

In SO2 program, costs did not appear minimized.

-

One possible explanation is other factors / constraints which also distort behavior in this sector.

-

Fowlie (2009) looks at one particularly obvious and important one: electricity regulation.

Electricity regulation

-

Historically electric power was entirely vertically integrated, and believed to be a natural monopoly.

-

Cost overruns/ poor investments in 70's and 80's lead people to reconsider this

-

Realization that while distribution was a natural monopoly (probably...), electric power generation need not be

-

For a recent review of experience with deregulation, see Borenstein and Bushnell (2015)

-

Fowlie says by 2001, 19 states had deregulated.

- B&B note that this is a more continuous measure

How regulation works

"Regulated" markets:

- firms make investments to keep the lights on

- regulator reviews these, and sets electricity prices such that "plants are guaranteed to earn a rate of return on prudent investments"

- including pollution abatement equipment.

"Deregulated" markets

- plants bid output into an auction.

- if bid is less than the market clearing price, it is dispatched (and recieves clearing price)

- firms make investments in order to to maximize profits

Dispatch curve

- high fixed cost, low variable "baseload" plants run all the time

- low fixed, high variable cost "peakers" only run during high demand

Why would regulation affect the cost effectiveness of compliance decisions?

-

Regulation tied to capital (Averch and Johnson 1962)

-

General lack of price incentives (Fabrizio, Rose and Wolfram AER)

-

Political incentives (Cicala 2015)

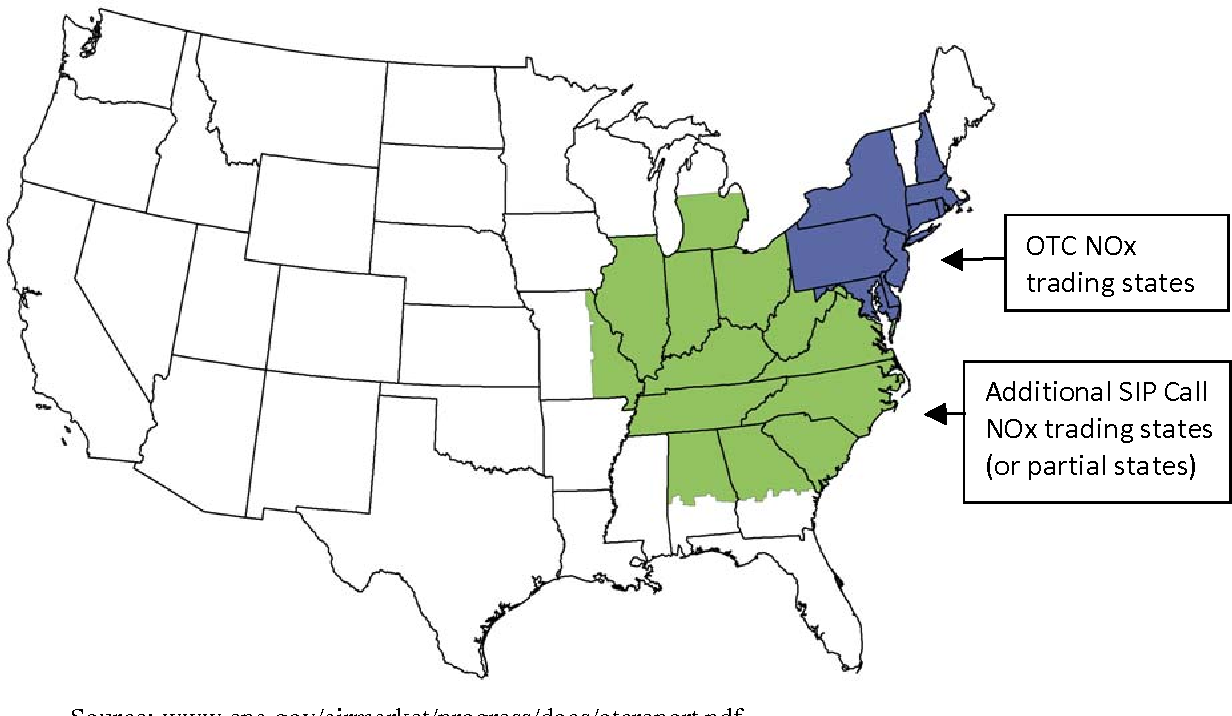

Fowlie studies the NOx Budget Program

-

NOx is a precursor for tropospheric ozone (O3)

- known to have severe health affects at high levels

-

19 eastern states covered

Important feature:

- even though baseline levels and marginal damages varied considerably across states, regulation was uniform across states

- 1 permit had same value everywhere.

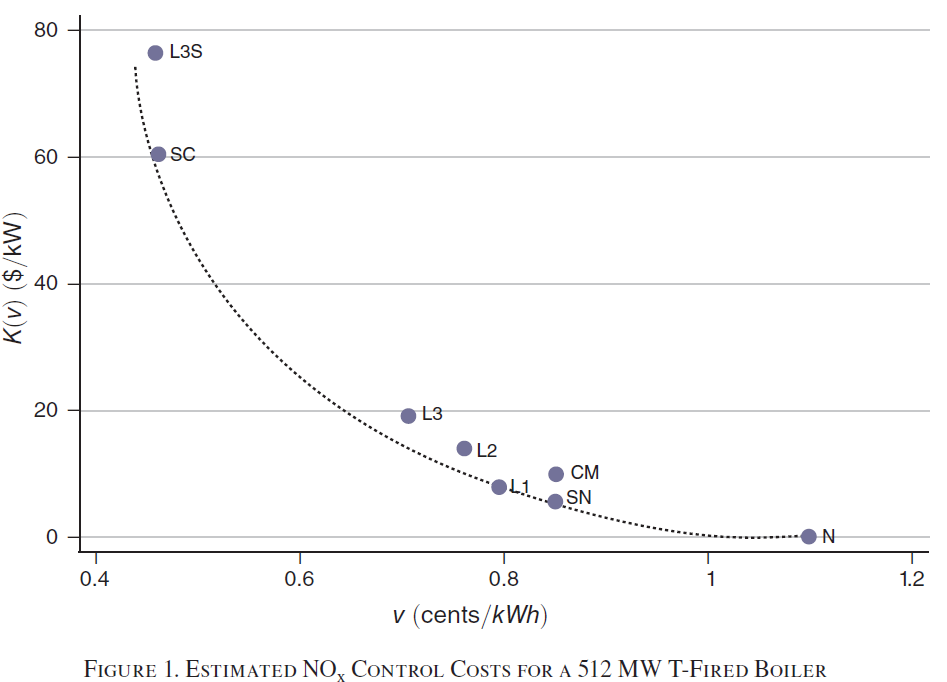

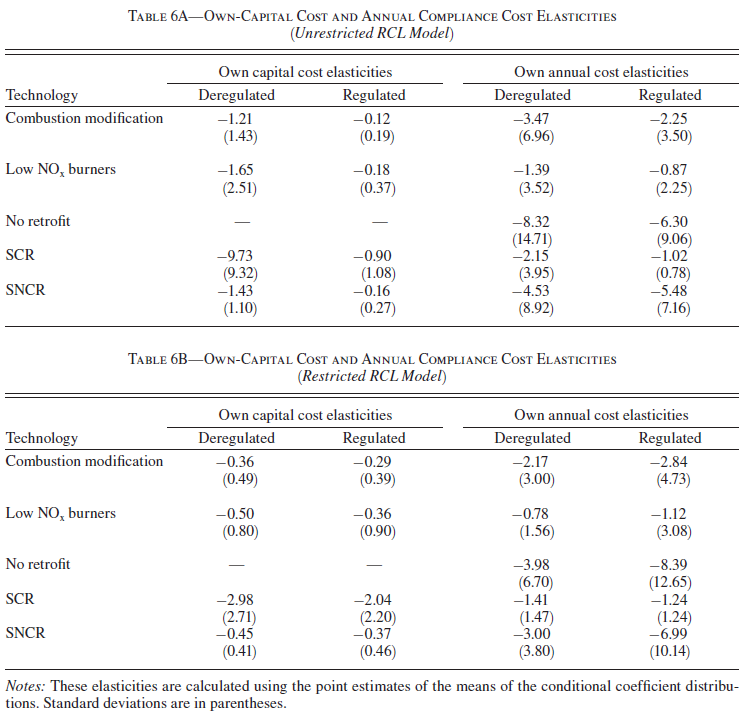

Different compliance options available to firms

- firms have tradeoff between capital costs and variable costs

Research Question

Broad:

How do pre-existing market distortions affect performance of cap-and-trade?

Specific:

-

Has heterogeneity in electricity market regulation affected how coal plant managers chose to comply with a regional NOx emissions trading program?

-

What were the environmental implications?

What is the empirical strategy?

Says "ideally coal generators would be randomly assigned to different regulatory regimes"

Instead relies on interstate variation in electricity market regulation (all covered under the same CAT program)

Program States

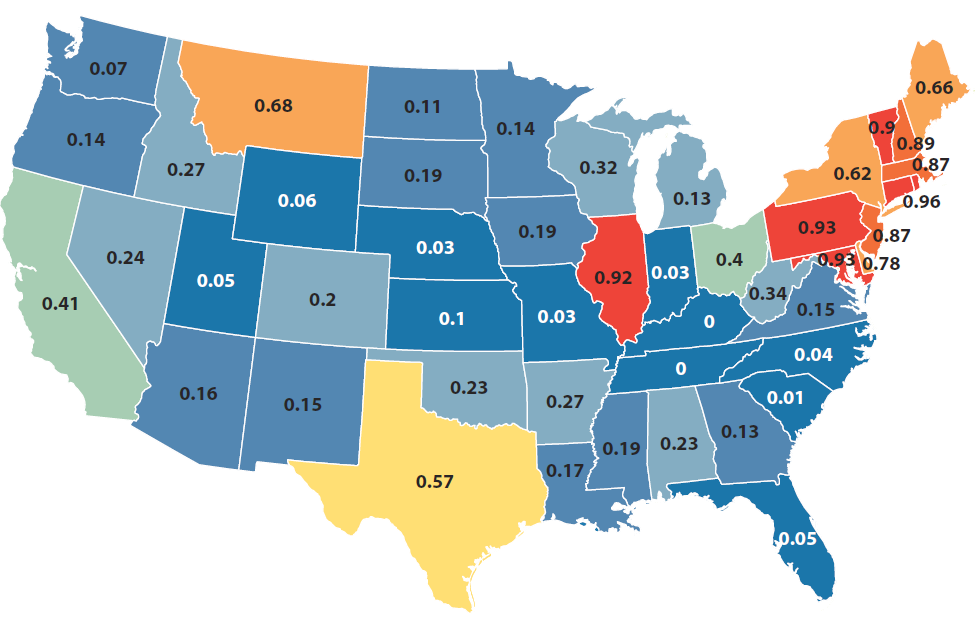

Merchant generation share by state (2015)

What do you think of this empirical strategy?

- is it believable?

- what would you worry about?

- what are Fowlie's arguments that you shouldn't worry?

Says this is viable for three reasons:

- Restructuring entirely determined pre NBP

- Restructuring driven by having high electricity prices.

- is this helpful?

- Plants compliance options similar across regulated and non-regulated states

Still, at the end of the day, comparison is between northern states with high prices (deregulated) and southern states with low prices (regulated). Up to author to convince us that's still informative.

Data

-

702 generating units

-

doesn't observe: variable or fixed costs, or beliefs about resulting emissions from different choices

What does she do?

How does this compare to what Carlson et al did?

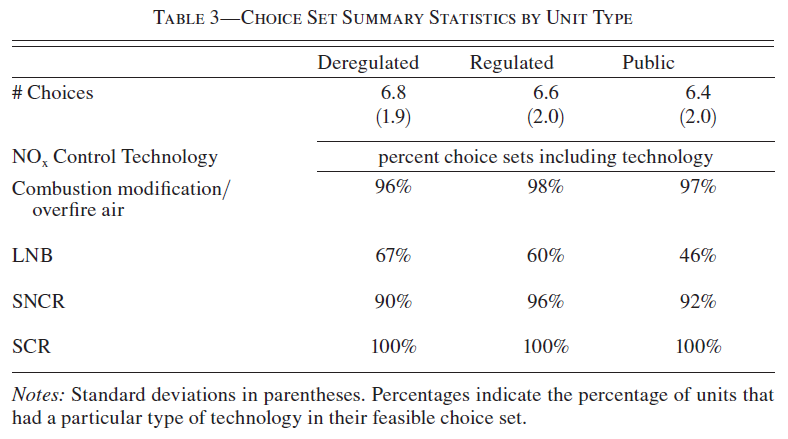

Summary stats

-

Show that regulated firms made different decisions

- no idea why this is done in pie charts

-

Then shows that compliance options and costs across the two look basically the same

- This motivates jumping to a restrictive model

What econometric techniques are employed?

-

What are the main estimating equations?

-

Why not OLS here?

Assume firms face the following (latent) cost structure

- firms $n$ with $J_n$ compliance options (assumed)

-

capital costs $K_{nj}$

-

variable costs $v_{nj}$ a function of permit price and (fixed?) output

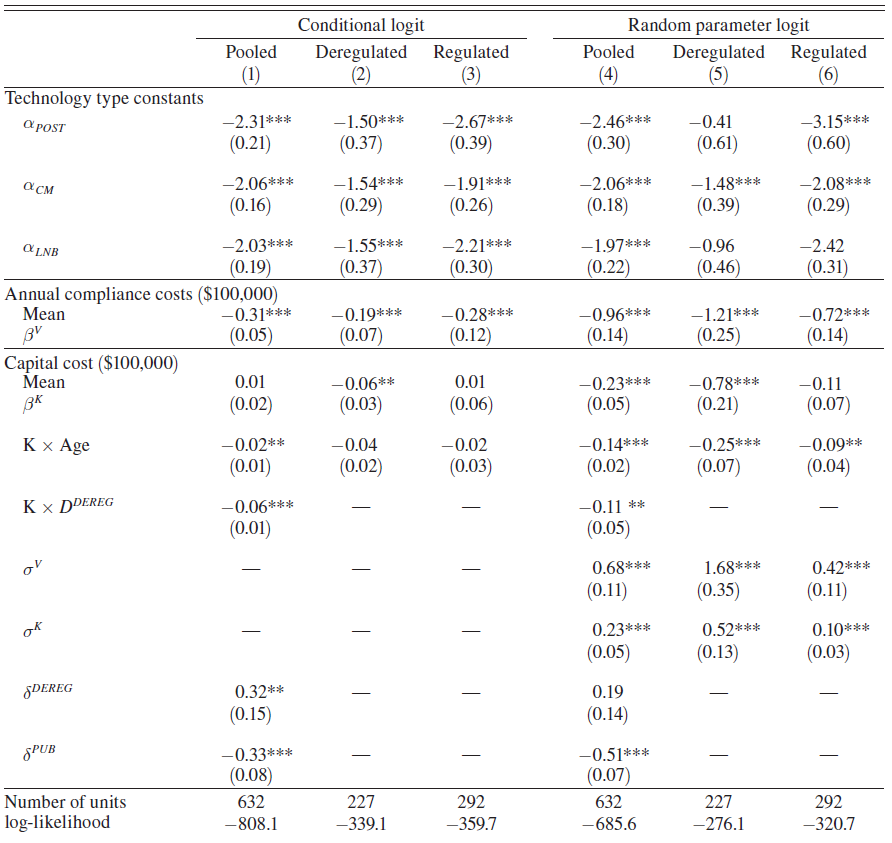

Goal of paper is to test if $\beta^v_n$ and $\beta^k_n$ differ for regulated and deregulated firms.

How does she do this?

- Pooled with interaction terms

- Separately with a comparison of relative significance across models

Conditional Logit

Probability the $n$ unit chooses compliance option $i$:

What are the limitations of this model?

-

Conditional on $X$, choice probabilities are the same, and errors are assumed independent

- Fowlie says other factors that vary unobservably across facilities might affect tastes

-

Panel nature of the data

- Same firm makes (presumably) correlated decisions across multiple plants/ boilers.

What were the other options here?

Random Coefficient Logit

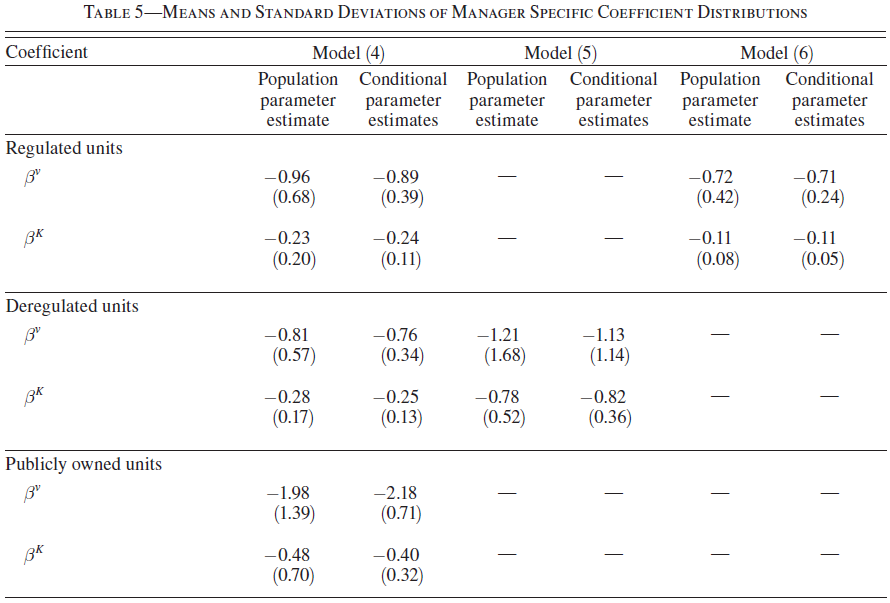

Assume tastes for capital ($\beta^v$) and capital ($\beta^K$) are distributed bivariate normal, and estimate the mean and variance of that distribution.

Draws from this distribution are assumed constant within manager $m$ across $T_m$ units.

Unconditional probabilities recovered by integrating over distribution of $\beta$

Let $b$ and $\Omega$ define the vector of coefficient means and variances.

Parameters then chosen to maximize:

How to actually do this

Estimated with simulated MLE

-

guess $b$ and $\omega$

-

for each manager take 1000 draws to calculate the integrand in $l(b,\Omega)$

-

Search over parameters to maximize likelihood of observed choices across all managers

What identifies $b$ and $\Omega$?

Recovering manager-specific parameters

-

in estimation, likelihood of each manager's choices based on 1000 draws from same distribution.

-

Fowlie then attempts to recover where in that distribution each manager's draw was given observed choices

-

Trick is to apply Bayes Rule

$$P(A|B) = \frac{P(B|A) P(A)}{P(B)}$$

Can write likelihood of type as function of choices

(conditional on estimates)

-

first term you get from CL formula for a given $\beta$

-

second term ($f$) recovered already during estimation

-

denominator can be obtained from simulation

- (or in theory is data if you believe $f$ is right)

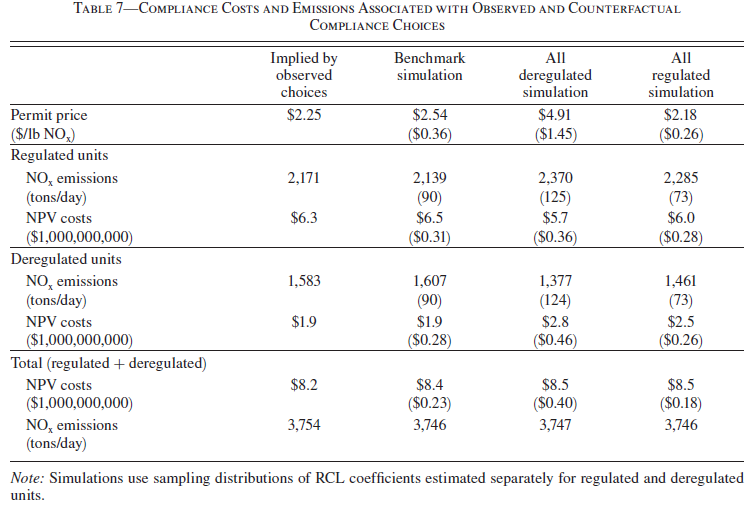

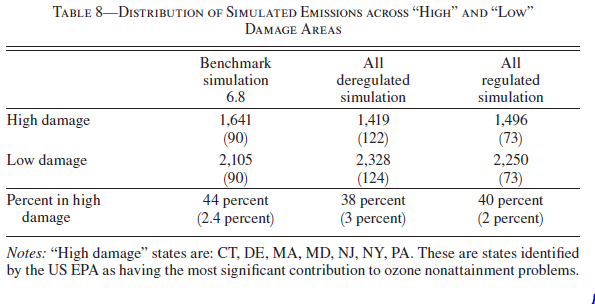

Takeaways

- overlapping, ostensibly unrelated, regulations/ policies can hinder eachother's efficacy

- in this case, rate of return regulation lead to different compliance costs

- this in turn altered location of emissions, which reduced the efficiency of the program

- note this could have gone either way!

- if correlation between damage and regulation was positive